Cardholder Agreement Important – Please Read Carefully

This Cardholder Agreement contains an Arbitration Clause requiring all claims to be resolved by way of binding arbitration.

Terms and Conditions

This Cardholder Agreement (“Agreement”) sets forth the terms and conditions under which the Everee Visa® Pay Card and virtual Card collectively known in this Agreement as (“Card”) has been issued to you by The Bancorp Bank, N.A., Member FDIC (“Issuer”). By accepting and using the Card, you agree to be bound by the terms and conditions contained in this Agreement. “Card Account” means the records we maintain to account for the value of claims associated with the Card. “You” and “your” mean the person or persons who have received the Card and are authorized to use the Card as provided for in this Agreement. “We,” “us,” and “our” mean the Issuer, our successors, affiliates, or assignees, and as applicable, the Program Manager. “Program Manager” means Everee, the entity providing certain services for servicing and/or managing the Card program on our behalf. “Program Sponsor” means the employer responsible for directly or indirectly sponsoring and making the Card available to you for the payment of wages, salary, or other employee compensation on a recurring basis. You acknowledge and agree that the value available in the Card Account is limited to the funds that have been loaded onto the Card Account. You agree to sign the back of the Card immediately upon receipt. The expiration date of the Card is identified on the back of your Card. The Card is a prepaid card. The Card is not connected in any way to any other account. The Card is not a credit card. The Card is not for resale. You will not receive any interest on your funds in the Card Account. The Card will remain the property of the Issuer and must be surrendered upon demand. The Card is nontransferable, and it may be canceled, repossessed, or revoked at any time without prior notice subject to applicable law. The Card is not designed for business use, and we may close your Card if we determine that it is being used for business purposes. We may refuse to process any transaction that we believe may violate the terms of this Agreement.

Write down your Card number and the customer service phone number provided in this Agreement on a separate piece of paper in case your Card is lost, stolen, or destroyed. Keep the paper in a safe place. Please read this Agreement carefully and keep it for future reference.

Customer Service

For customer service or additional information regarding your Card, please contact “Customer Service” at the “Address,” “Phone Number” or “Website” below:

Everee Visa Pay Card

PO Box 17170

Salt Lake City, UT 84117

Everee.com

(833) 313-6776 Toll Free

Customer Service agents are available to answer your calls:

Monday through Friday, 6 a.m. to 6 p.m. MT

Saturday, Sunday, and holidays closed.

Our business days are Monday through Friday, excluding federal holidays, even if we are open. Any references to “days” found in this Agreement are calendar days unless indicated otherwise. From time to time, we may monitor and/or record telephone calls between you and us to assure the quality of our customer service or as required by applicable law.

Activating and Registering your Card

Warning regarding unverified Cards: It is important to register your prepaid account as soon as possible. Until you register your account, and we verify your identity, we are not required to research or resolve any errors regarding your account. To register your account, go to our mobile app or call our Phone Number. We will ask you for identifying information about yourself (including your full name, address, date of birth, and Social Security Number or government-issued identification number), so that we can verify your identity.

Important Information About Procedures For Opening A New Card Account: To help the government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens a Card Account. What this means for you: When you open a Card Account, we will ask for your name, address, date of birth, and other information that will allow us to identify you. We may also ask to see a copy of your driver’s license or other identifying documents.

You must activate and register your physical and/or virtual Card before it can be used. To do so, please visit our mobile app or call Customer Service. By activating the Card or by retaining, using or authorizing the use of the Card, you represent and warrant to us that: (i) you are at least 16 years of age (or older if you reside in a state where the majority age is older); (ii) you are a U.S. citizen or legal alien residing in the fifty (50) states of the United States (“U.S.”) or the District of Columbia; (iii) you have provided us with a verifiable U.S. street address (not a P.O. Box); (iv) the personal information that you provide to us in connection with the Card is true, correct and complete; (v) you received a copy of this Agreement and agree to be bound by and to comply with its terms; and (vi) you accept the Card.

Personal Identification Number (“PIN”)

You will not receive a PIN with your Card. However, you will be prompted to select a PIN when you activate your Card.

You should not write or keep your PIN with your Card. Never share your PIN with anyone. When entering your PIN, be sure it cannot be observed by others and do not enter your PIN into any terminal that appears to be modified or suspicious. If you believe that anyone has gained unauthorized access to your PIN, you should advise us immediately following the procedures in the paragraph labeled “Your Liability for Unauthorized Transfers.”

Authorized Card Users

You are responsible for all authorized transactions initiated and fees incurred by use of your Card. If you permit another person to have access to your Card or Card number(s), we will treat this as if you have authorized such use and you will be liable for all transactions and fees incurred by those persons. You are wholly responsible for the use of each Card according to the terms and conditions of this Agreement.

Loading and Using the Card

The Program Sponsor may load your Card via the methods and with the limitations set forth below. Personal checks, cashiers’ checks, and money orders sent to the Issuer are not an acceptable form of loading. At our discretion, we may allow a load payment in excess of the limits disclosed below, including the maximum value limit, to post to your Card Account. However, if such a load payment is permitted to post to your Card Account on one occasion, there is no guarantee that any load(s), in any form, in excess of the disclosed limit will be permitted in the future. All checks and money orders sent to the Issuer for Card loading will be returned unless the full amount may be applied towards a negative balance, in which case the check or money order may or may not be loaded to the Card at the discretion of the Issuer.

With your PIN, you may use your Card to obtain cash from any Automated Teller Machine (“ATM”) or any Point-of-Sale (“POS”) device, as permissible by a merchant that bears the Visa® or MoneyPass® acceptance mark. All ATM transactions are treated as cash withdrawal transactions. You may use your Card at an ATM and withdraw funds from a participating bank (over the counter withdrawal). Any funds withdrawn from a POS device will be subject to the maximum amount that can be spent on your Card per day.

These are the limits associated with your Card:

Transaction Type | Frequency and/or Dollar Limits |

Max Balance | $50,000.00 |

Direct Deposit | Five (5) times per day; up to $10,000.00 per day |

Cash Withdrawal (ATM)* | Three (3) times per day, $255.00 per transaction; up to $510.00 per day |

Cash Withdrawal (Over the Counter) | $5,000.00 per transaction; up to $5,000.00 per day |

Cash Withdrawal* (ATM, OTC, cashback at POS) | $5,000 per day |

Card Purchases (Signature) | $5,000.00 per transaction, up to $5,000.00 per day |

Card Purchases (PIN) | $5,000.00 per transaction, up to $5,000.00 per day |

Total Card Spend (ATM, purchases, OTC, cashback at POS) | $5,510.00 per day |

Outbound ACH** | Three (3) times per day up to $5,000.00 per day |

*ATM owner-operators and participating banks may impose their own lower limits on cash withdrawals. **Third party money transfer providers may impose their own limits. | |

You may use your Card to purchase or lease goods or services everywhere Visa debit cards, Maestro cards, or MoneyPass cards are accepted as long as you do not exceed the available value of your Card Account and other restrictions (see examples described below) do not apply. Some merchants do not allow cardholders to conduct split transactions where you would use the Card as partial payment for goods and services and pay the remainder of the balance with another form of legal tender. If you wish to conduct a split transaction and it is permitted by the merchant, you must tell the merchant to charge only the exact amount of funds available on the Card Account to the Card. You must then arrange to pay the difference using another payment method. Some merchants may require payment for the remaining balance in cash. If you fail to inform the merchant that you would like to complete a split transaction prior to swiping your Card, your Card is likely to be declined.

If you use your Card number without presenting your Card (such as for a mail order, telephone, or Internet purchase), the legal effect will be the same as if you had used the Card itself. Card Account restrictions include but are not limited to: restricted geographic or merchant locations where there is a higher risk of fraud or illegal activity; restrictions to comply with laws or prevent our liability; and other restrictions to prevent fraud and other losses. For security reasons, we may, with or without prior notice, limit the type, amount, or number of transactions you can make on your Card. You may not use your Card for illegal online gambling or any other illegal transaction. We may increase, reduce, cancel, or suspend any of the restrictions or add new ones at any time. Your Card cannot be redeemed for cash.

Each time you use your Card, you authorize us to reduce the available value of your Card Account by the amount of the transaction and any applicable fees. You are not allowed to exceed the available amount in your Card Account through an individual transaction or a series of transactions. Nevertheless, if a transaction exceeds the available balance of funds on your Card, you shall remain fully liable to us for the amount of the transaction and any fees, if applicable. You are responsible for keeping track of the available balance of your Card Account. Merchants generally will not be able to determine your available balance. It’s important to know your available balance before making any transaction.

Preauthorized Transfers

Your Card Account cannot be used for preauthorized automated clearinghouse “ACH” debits or Card transactions from merchants, Internet service or other utility service providers. If presented for payment, preauthorized transfers may be declined and payment to the merchant or provider will not be made. You are not authorized to provide the Issuer’s bank routing and account number to anyone other than for use in direct deposit. Nevertheless, we have no obligation to stop any preauthorized transfer, and your Card Account may be subject to closure if preauthorized transfers are attempted or completed.

If you use your Card at an automated fuel dispenser (“pay at the pump”), the transaction may be preauthorized for an amount up to $100.00 or more. If your Card is declined, even though you have sufficient funds available, you should pay for your purchase inside with the cashier. If you use your Card at a restaurant, a hotel, for a car rental purchase, or for similar purchases, the transaction may be preauthorized for the purchase amount plus up to 20% or more to ensure there are sufficient funds available to cover tips or incidental expenses incurred. A preauthorization will place a “hold” on those available funds until the merchant sends us the final payment amount of your purchase. Once the final payment amount is received, the preauthorized amount on hold will be removed. It may take up to seven (7) days for the hold to be removed. During the hold period, you will not have access to the preauthorized amount.

You do not have the right to stop payment on a single purchase or payment transaction originated by use of your Card. If you authorize a transaction and then fail to make the purchase of that item as planned, the approval may result in a hold for that amount of funds for up to thirty (30) days. All transactions relating to car rentals may result in a hold for that amount of funds for up to sixty (60) days.

Non-Visa Debit Transactions

Certain protections and rights applicable only to Visa debit transactions as described in this Agreement will not apply to transactions processed on another network. If you do not enter a PIN, transactions may be processed as either a Visa debit transaction or on another network transaction. Should you choose to use a non-Visa network when making a transaction without a PIN, different terms may apply.

To initiate a Visa debit transaction at the POS, swipe the Card through a POS terminal, sign the receipt, or provide the 16-digit Card number for a mail order, telephone, or Internet purchase. To initiate a non-Visa debit transaction at the POS, enter the PIN at the POS terminal or provide the 16-digit Card number after clearly indicating a preference to route the transaction as a non-Visa debit transaction for certain bill payment, mail order, telephone, or Internet purchases.

Returns and Refunds

If you are entitled to a refund for any reason for goods or services obtained with the Card, you agree to accept credits to the Card for such refunds and agree to the refund policy of that merchant. Any Merchant disputes, returns, or refunds must be addressed and handled directly with the merchant from whom the transaction posted, or those goods or services were provided. We are not responsible for the delivery, quality, safety, legality or any other aspects of goods or services you purchase from others with a Card.

Card Expiration and Replacement

Your Card will expire no sooner than the date printed on the back of it. The funds on the Card do not expire. You will not be able to use your Card after the expiration date. You may request a replacement Card at no cost to you by calling Customer Service. A replacement Card will automatically be mailed to you prior to the expiration of the soon-to-expire Card.

If you need to replace your Card for any reason, please call Customer Service to request a replacement Card. You will be required to provide personal information which may include your 16-digit Card number, full name, transaction history, copies of accepted identification, etc. There may be a fee for replacing a lost, stolen, or damaged Card or for expedited delivery of an additional Card; for more information about the delivery options and applicable fees, see the section labeled “Fee Schedule.”

Foreign Transactions

You may use the Card to purchase or lease goods or services everywhere Visa debit cards, Maestro cards, or MoneyPass cards are accepted as long as you do not exceed the available value in the Card Account, and other restrictions (see examples described below) do not apply. If you make a purchase in a currency other than the currency in which the Card was issued, the amount deducted from the funds will be converted by Visa into an amount in the currency of the Card. The exchange rate between the transaction currency and the billing currency used for processing international transactions is a rate selected by Visa from the range of rates available in wholesale currency markets for the applicable central processing date, which may vary from the rate Visa itself receives, or the government-mandated rate in effect for the applicable central processing date.

Receipts

You should get a receipt at the time you make a transaction using your Card. You may need to retain receipts in order to verify or reconcile your transactions.

Negative Balances

If the available balance in the Account is insufficient to cover any authorized payment or withdrawal, we can refuse to honor the payment or withdrawal. You are not permitted to conduct transactions that bring your Account balance negative. If the Account balance should become negative for any reason, a deposit or deposits must be immediately made to cover the negative balance. If the Account has a negative balance for ninety (90) calendar days, it may be closed. You will remain liable to us for any amounts owed due to negative balances, and we reserve the right to pursue all remedies under law to resolve any negative balance, including setting off the balance with other funds you may hold with the Issuer.

Periodic Statement

You will get a monthly account statement (unless there are no transfers in a particular month. In any case you will get a statement at least quarterly). Periodic statements are available on our website at https://app.everee.com/.

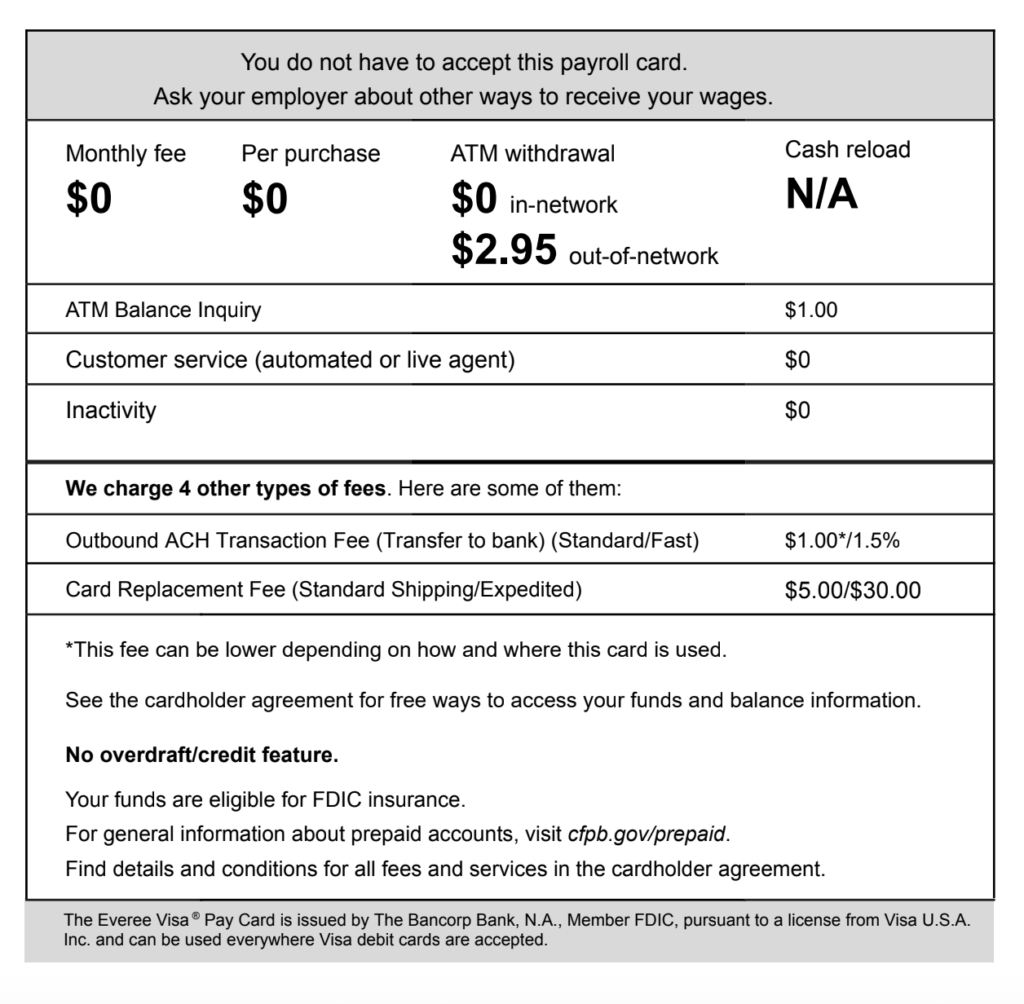

Fee Schedule

All fee amounts will be withdrawn from your Card Account and will be assessed as long as there is a remaining balance on your Card Account, except where prohibited by law. Any time your remaining Card Account balance is less than the fee amount being assessed, the balance of your Card Account will be applied to the fee amount resulting in a zero balance on your Card Account.

List of all fees for the Everee Visa® Pay Card

All Fees | Amount | Details |

Get Started | ||

Card purchase | $0 | |

Monthly usage | ||

Monthly fee | $0 | |

Add money | ||

Direct deposit | $0 | |

Spend | ||

Purchases (PIN/POS) | $0 | |

Outbound ACH Transaction Fee (Transfer to bank) | $1.00 | This is our fee per transaction. The first 2 transactions are free per rolling 30-day period and then this fee is assessed. |

Fast Outbound ACH Transaction Fee (Transfer to bank) | 1.5% of transfer amount | This is our fee per transaction when you choose to use the Fast Transfer option to transfer funds off your card. Such fast transfers will not count against the two free transfers you have available, as described above. This fee will be assessed in favor of the regular Outbound ACH Transaction Fee (if applicable). If submitted before 1:00 PM ET, your money will arrive on the same day; if received after the last window, your money will arrive on the next business day. |

Get Cash | ||

ATM withdrawal (in-network) | $0 | “In-network” refers to ATMs in the MoneyPass network. You may also be charged a fee by the ATM operator, including for a balance inquiry, even if you do not complete a transaction. |

ATM withdrawal (out-of-network) | $2.95 | This is our fee per transaction. “Out-of-network” refers to all the ATMs outside of the MoneyPass ATM Network. You may also be charged a fee by the ATM operator, even if you do not complete a transaction. |

Information | ||

Customer service (automated) | $0 | No fee for calling our automated customer service line, including balance inquiries. |

Customer service (live agent) | $0 | No fee for connecting to our live agents. |

ATM balance inquiry (domestic) | $1.00 | This is our fee charged per inquiry. You may also be charged a fee by the ATM operator, even if you do not complete a transaction. To view your balance for free, visit the Everee Mobile App. |

Using your card outside the U.S. | ||

ATM Withdrawal (International) | $2.95 | This is our fee per transaction. You may also be charged a fee by the ATM operator, even if you do not complete a transaction. |

ATM Balance Inquiry (International) | $1.00 | This is our fee charged per inquiry. You may also be charged a fee by the ATM operator, even if you do not complete a transaction. To view your balance for free, visit the Everee Mobile App. |

Other | ||

Replacement card fee | $5.00 | This is our fee, per replacement request and is assessed if you request a new card, for lost, stolen, or damaged reason. 7 – 10 business days for delivery. |

Expedited card replacement fee | $25.00 | This is our fee per request when expediting a Card replacement. Expedited replacement in 2 business days for delivery. This fee is in addition to the Replacement card fee. |

Your funds are eligible for FDIC insurance. Your funds will be held at or transferred to The Bancorp Bank, N.A. an FDIC-insured institution. Once there, your funds are insured up to $250,000 by the FDIC in the event The Bancorp Bank, N.A. fails, if specific deposit insurance requirements are met and your card is registered. See fdic.gov/deposit/deposits/prepaid.html for details. No overdraft/credit feature. Contact Everee Pay Card by calling (833) 313-6776 toll free, by mail at PO Box 17170 Salt Lake City, UT 84117 or visit everee.com. For general information about prepaid accounts, visit cfpb.gov/prepaid. If you have a complaint about a prepaid account, call the Consumer Financial Protection Bureau at 1-855-411-2372 or visit cfpb.gov/complaint. | ||

Confidentiality

We may disclose information to third parties about your Card or the transactions you make:

- Where it is necessary for completing transactions;

- In order to verify the existence and condition of your Card for a third party, such as a merchant;

- In order to comply with government agency, court order, or other legal or administrative reporting requirements;

- If you consent by giving us your written permission;

- To our employees, auditors, affiliates, service providers, or attorneys as needed; or

- As otherwise necessary to fulfill our obligations under this Agreement.

Our Liability for Failure To Complete Transactions

If we do not properly complete a transaction from your Card on time or in the correct amount according to our Agreement with you, we will be liable for your losses or damages. However, there are some exceptions. We will not be liable, for instance:

- If through no fault of ours, you do not have enough funds available on your Card to complete the transaction;

- If a merchant refuses to accept your Card;

- If an ATM where you are making a cash withdrawal does not have enough cash;

- If an electronic terminal where you are making a transaction does not operate properly, and you knew about the problem when you initiated the transaction;

- If access to your Card has been blocked after you reported your Card lost or stolen;

- If there is a hold or your funds are subject to legal or administrative process or other encumbrance restricting their use;

- If we have reason to believe the requested transaction is unauthorized;

- If circumstances beyond our control (such as fire, flood, or computer or communication failure) prevent the completion of the transaction, despite reasonable precautions that we have taken; or

- Any other exception stated in our Agreement with you.

Your Liability for Unauthorized Transfers

Tell us AT ONCE if you believe your Card or code has been lost or stolen, or if you believe that an electronic fund transfer has been made without your permission using information from your Card. Telephoning is the best way of keeping your possible losses down. You could lose all the money in your Card Account. If you tell us within 2 business days after you learn of the loss or theft, you can lose no more than $50 if someone used your Card or Card Account without your permission. If you do NOT tell us within 2 business days after you learn of the loss or theft of your Card or code, and we can prove we could have stopped someone from using your Card or code without your permission if you had told us, you could lose as much as $500.

Also, if your periodic statement shows transfers that you did not make, including those made by Card, code, or other means, tell us at once. If you do not tell us within 60 days after the earlier you accessed your Card Account or the date we FIRST sent a periodic statement to you (if applicable), you may not get back any money you lost after the 60 days if we can prove that we could have stopped someone from taking the money if you had told us in time. If a good reason (such as a long trip or a hospital stay) kept you from telling us, we will extend the time periods.

Under Visa Core Rules, your liability for unauthorized Visa debit transactions on your Card Account is $0.00 if you are not negligent or fraudulent in the handling of your Card. This reduced liability does not apply to certain commercial card transactions, transactions not processed by Visa, or to anonymous prepaid cards (until such time as the identity of the cardholder has been registered with us). You must notify us immediately of any unauthorized use.

Information About Your Right to Dispute Errors

In Case of Errors or Questions About Your Card Account call us, write us, or email us at the Customer Service contact information above as soon as you can, if you think an error has occurred in your Card Account. We must allow you to report an error until 60 days after the earlier of the date you electronically access your account, if the error could be viewed in your electronic history, or the date we sent the FIRST written history on which the error appeared. You will need to tell us:

Your name and Card number.

Why you believe there is an error, and the dollar amount involved.

Approximately when the error took place.

If you tell us orally, we may require that you send us your complaint or question in writing within 10 business days. We will determine whether an error occurred within 10 business days after we hear from you and will correct any error promptly. If we need more time, however, we may take up to 45 days to investigate your complaint or question. If we decide to do this, we will credit your account within 10 business days for the amount you think is in error, so that you will have the money during the time it takes us to complete our investigation. If we ask you to put your complaint or question in writing and we do not receive it within 10 business days, we may not credit your account.

For errors involving new accounts, point-of-sale, or foreign-initiated transactions, we may take up to 90 days to investigate your complaint or question. For new accounts, we may take up to 20 business days to credit your account for the amount you think is in error. We will tell you the results within three business days after completing our investigation. If we decide that there was no error, we will send you a written explanation. You may ask for copies of the documents that we used in our investigation.

English Language Controls

Any translation of this Agreement is provided for your convenience. The meanings of terms, conditions and representations herein are subject to definitions and interpretations in the English language. Any translation provided may not accurately represent the information in the original English.

Other Miscellaneous Terms

Your Card and your obligations under this Agreement may not be assigned. We may transfer our rights under this Agreement. Use of your Card is subject to all applicable rules and customs of any clearinghouse or other association involved in transactions. We do not waive our rights by delaying or failing to exercise them at any time. If any provision of this Agreement shall be determined to be invalid or unenforceable under any rule, law, or regulation of any governmental agency, local, state, or federal, the validity or enforceability of any other provision of this Agreement shall not be affected. This Agreement will be governed by the law of the State of South Dakota except to the extent governed by federal law.

Legal Processes Affecting Accounts

If legal action such as a garnishment, levy, or other state of federal legal process (“Legal Process”) is brought against your Card Account, we may refuse to permit (or may limit) withdrawals or transfers until the Legal Process is satisfied or dismissed. Regardless of the terms of such garnishment, levy or other state or federal process, we have first claim to any and all funds in your Card Account. We will not contest on your behalf any such Legal Process and may take action to comply with such Legal Process as we determine to be appropriate in the circumstances without liability to you, even if any funds we may be required to pay out leaves insufficient funds to pay a transaction that you have authorized. Prior to making any funds payout required by Legal Process, we may first satisfy any fees, charges or other debts owed to us under this Agreement by charging these expenses to your Card Account. If we incur any expense, including, but not limited to administrative costs and reasonable attorney fees, in responding to Legal Process related to your Card Account, we may charge such expenses to your Card Account without prior notice, to the extent permitted by applicable law.

Amendment and Cancellation

We may amend or change the terms and conditions of this Agreement at any time. You will be notified of any change in the manner provided by applicable law prior to the effective date of the change. However, if the change is made for security purposes, we can implement such change without prior notice. We may cancel or suspend your Card or this Agreement at any time. You may close your Card Account by contacting Customer Service. The termination of your Card or this Agreement will not affect any of our rights or your obligations arising under this Agreement prior to termination.

In the event your Card Account is canceled, closed, or terminated for any reason; you may request that the unused balance be refunded to you. For security purposes, you may be required to supply identification and address verification documentation prior to being issued a refund. In the event this Card program is canceled, closed, or terminated, we will send you prior notice in accordance with applicable law. The Issuer reserves the right to refuse to return any unused balance amount less than $1.00. The time frame for processing and delivery of any refund depends on the method you select to receive it. Refund delivery methods may include, but not be limited to, mailing a paper check to you, or receiving an electronic check by email.

Arbitration

This Arbitration Clause sets forth the procedures for resolving a Claim under this Agreement. As used in this Arbitration Clause, a “Claim” is any preexisting, present or future claim, dispute, or controversy between you and us arising out of or relating directly or indirectly in any way to this Agreement. The term “Claim” has a very broad meaning and includes, by way of example and not limitation, disputes concerning: (i) the acquisition, use, or balance of your Card Account; (ii) advertisements, promotions or oral or written statements related to the Card Account (iii) a dispute based on a federal or state statute or local ordinance; (iv) data breach or privacy claims arising from or relating directly or indirectly to the disclosure by us of any nonpublic personal information about you; and (v) the relationships between you and us arising from this Agreement or any of the foregoing. Notwithstanding the foregoing, a “Claim” does not include (i) the exercising of any self-help or non-judicial remedies by you or us, meaning actions you or we can take that do not involve court action. Examples of this include setoff rights or enforcement of our security interest in your Card Account, (ii) disputes regarding a person’s authority to act on your Card Account and disputes regarding ownership of funds and other legal matters dealing with “legal process” or “legal proceedings and disputes”; and (iii) obtaining provisional or ancillary remedies including, but not limited to, attachment, garnishment, interpleader or the appointment of a receiver by a court of appropriate jurisdiction.

This Arbitration Clause provides that all Claims shall be FINALLY and EXCLUSIVELY resolved by binding individual arbitration, unless excepted or opted out in accordance with the terms below.

By not opting out according to the terms below, you acknowledge that:

YOU AND WE WILL BE BOUND BY THIS CLAUSE TO ARBITRATE ANY CLAIM IF YOU OR WE ELECT ARBITRATION, UNLESS THE CLAIM IS BROUGHT IN OR REMOVED TO SMALL-CLAIMS COURT PURSUANT TO THIS ARBITRATION CLAUSE;

NEITHER PARTY WILL HAVE THE RIGHT TO A JURY TRIAL OR TO ENGAGE IN DISCOVERY, EXCEPT AS PROVIDED FOR IN THE AAA CODE OF PROCEDURE; AND

YOU AND WE WILL NOT BE ABLE TO BRING OR BE A CLASS MEMBER IN A CLASS ACTION, PRIVATE ATTORNEY GENERAL ACTION OR OTHER REPRESENTATIVE ACTION IN COURT OR IN ARBITRATION (“Class Action Waiver”).

Arbitration: In arbitration, a neutral third-party arbitrator resolves Claims on an individual basis. Arbitrations under this Arbitration Clause will be made pursuant to a transaction involving interstate commerce and shall be governed by the Federal Arbitration Act (“FAA”) (9 U.S.C. 1-16). An arbitration of a Claim will be conducted by the American Arbitration Association (“AAA”) under its rules; if AAA cannot serve and we do not agree on an alternative arbitrator, a court with jurisdiction will select the arbitrator. For a copy of AAA procedures, to file a Claim, or for other information about this organization, contact AAA at 120 Broadway, Floor 21, New York, NY 10271, (1-800-778-7879), www.adr.org. We will pay the initial filing fee to commence arbitration and other fees we are required to pay by the AAA Rules, and any arbitration hearing that you attend shall take place in the federal judicial district of your residence. The arbitrator’s award shall be binding and final, except for any appeal rights under the FAA. Judgment on the arbitration award may be entered in any court having jurisdiction.

Alternative for Individual Claims: This Arbitration Clause does not affect your or our right to pursue individual Claims in small claims court (or your state’s equivalent court) if the court has jurisdiction over the dispute and the dispute remains in that court. If a party brings a Claim in arbitration, the other party may remove the Claim to small-claims court if the amount in controversy (exclusive of attorneys’ fees and costs if applicable law so provides) is properly within the jurisdiction of a small-claims court. The opposing party must provide notice of intent to remove to small-claims court within 30 days of receiving an arbitration demand from the other party. In any event, if the Claim is removed, appealed, or transferred from small-claims court to another court, it shall be subject to arbitration at the election of either party.

Enforceability: All disputes as to the scope, enforceability and validity of this Arbitration Clause shall be made exclusively by a court of competent jurisdiction.

Process: Before bringing a Claim in court or in arbitration, the complaining party must give the other party written notice of the Claim. If you are the complaining party, you must send the notice in writing (and not electronically) to PO Box 71337, Salt Lake City, UT 84171. You or your representative must sign the notice and must explain the nature of the Claim and any supporting information, such as your Card Account number and a contact information where you (or your representative) can be reached. If we bring a Claim, we will send a letter to you using the information we have on file for you. The receiving party will have 30 days to respond to the demand.

Opting out: If you do not wish to be bound by this Arbitration Clause, you must mail us a signed notice within 45 calendar days after you acquire or open the Card Account to PO Box 71337, Salt Lake City, UT 84171. We will need your name, address, telephone number and Card Account number. State that you “opt out” of arbitration. Opting out will not affect the other provisions of this Agreement. By opting out, you will have all options available under law to raise a dispute or Claim.

Survival: This Arbitration Clause shall survive: (i) termination of the Agreement by either party; (ii) the bankruptcy of any party; (iii) any transfer, sale or assignment, or any amounts owed on your Card Account, to any other person or entity; or (iv) closing of the Card Account. If any portion of this Arbitration Clause is deemed invalid or unenforceable, the remaining portions shall remain in force, except that: (A) If the Class Action Waiver is declared unenforceable in a proceeding between you and us with respect to a Claim that does not seek public injunctive relief, and that determination becomes final after all appeals have been exhausted, this entire Arbitration Clause (except for this sentence) shall be null and void in such proceeding; and (B) If a Claim is brought seeking public injunctive relief and a court determines that the restrictions in this Arbitration Clause prohibiting the arbitrator from awarding relief on behalf of third parties are unenforceable with respect to such Claim, and that determination becomes final after all appeals have been exhausted, the Claim for public injunctive relief will be determined in court and any individual Claims seeking monetary relief will be arbitrated. In such a case the parties will request that the court stay the Claim for public injunctive relief until the arbitration award pertaining to individual relief has been entered in court. In no event will a Claim for class-wide or public injunctive relief be arbitrated.

The Everee Visa ® Pay Card is issued by The Bancorp Bank, N.A., Member FDIC, pursuant to a license from Visa U.S.A. Inc. and can be used everywhere Visa debit cards are accepted.

This Cardholder Agreement is effective 05/2026

Rev. 12/2022

FACTS: WHAT DOES THE BANCORP BANK, N.A. DO WITH YOUR PERSONAL INFORMATION?

Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. |

What? | The types of personal information we collect, and share depend on the product or service you have with us. This information can include:

When you are no longer our customer, we continue to share your information as described in this notice. |

How? | All financial companies need to share customers’ personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons The Bancorp chooses to share; and whether you can limit this sharing. |

Reasons we can share your personal information | Does The Bancorp share? | Can you limit this sharing? |

For our everyday business purposes— such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus | Yes | No |

For our marketing purposes— to offer our products and services to you | Yes | No |

For joint marketing with other financial companies | No | We don’t share |

For our affiliates’ everyday business purposes— information about your transactions and experiences | No | We don’t share |

For our affiliates’ everyday business purposes— information about your creditworthiness | No | We don’t share |

For nonaffiliates to market to you | No | We don’t share |

QUESTIONS? Call us, toll-free, at (833) 313-6776 or email us at support@everee.com.

Who we are | |||

Who is providing this notice? | This notice is provided by The Bancorp Bank, N.A. | ||

What we do | |||

How does The Bancorp protect my personal information? | To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings. We also limit access to information to those employees for whom access is necessary. | ||

How does The Bancorp collect my personal information? | We collect your personal information, for example, when you

We also collect your personal information from others, such as credit bureaus, affiliates, or other companies. | ||

Why can’t I limit all sharing? | Federal law gives you the right to limit only

State laws and individual companies may give you additional rights to limit sharing. | ||

Definitions | |||

Affiliates | Companies related by common ownership or control. They can be financial and nonfinancial companies.

| ||

Nonaffiliates | Companies not related by common ownership or control. They can be financial and nonfinancial companies.

| ||

Joint marketing | A formal agreement between nonaffiliated financial companies that together market financial products or services to you.

| ||

Other Important Information | |

Vermont Residents:

| We will not disclose information about your creditworthiness to our affiliates and will not disclose your personal information, financial information, credit report, or health information to nonaffiliated third parties to market to you, other than as permitted by Vermont law, unless you authorize us to make those disclosures. |

Nevada Residents: | Nevada law requires that we provide you with the following contact information: Bureau of Consumer Protection, Office of the Nevada Attorney General, 555 E. Washington Ave., Suite 3900, Las Vegas, NV 89101; Phone number: 702-486-3132; email: agInfo@ag.nv.gov |

California Residents: | State general privacy laws permit consumers who are California residents to (a) ask a covered business which categories and pieces of personal information it collects and how the information is used; (b) request deletion of the information; (c) request correction of incorrect personal information and (d) opt out of the sale and sharing of such information. State general privacy laws have exemptions for either: (i) personal information collected, processed, shared, or disclosed by financial institutions pursuant to federal law or (ii) financial institutions in general as federal financial privacy law subject entities. To contact us with questions about our compliance with state general privacy laws, call 1-833-981-1080; visit our website: https://www.thebancorp.com/ccpa-web-form/or write to: The Bancorp/CCPA, PO Box 5017, Sioux Falls, SD 57117-5017. |